- EN

Notes to the consolidated annual financial statements

Ina Invest Holding Ltd (the Company) is a Swiss company domiciled at Binzmühlestrasse 11, Zurich, Switzerland. The Company’s consolidated financial statements cover the Company and its subsidiaries (referred to collectively as “the Group” or “Ina Invest”). The individual companies are to be considered group companies.

The Group’s business activities comprise developing and building of real estate and construction projects of all kinds, planning and completion of new buildings and conversions of real estate held by Ina Invest, as well as holding, managing, renting and brokering of real estate.

For the first time, the consolidated financial statements were prepared in accordance with the full Accounting and Reporting Recommendations (Swiss GAAP FER), including Swiss GAAP FER 31 “Complementary recommendations for listed companies” and provides a true and fair view of the Group’s assets, financial situation and earnings. The consolidated financial statements comply with the provisions of Swiss law. The Group discloses the additional information required for real estate companies by the Swiss stock exchange (SIX Swiss Exchange) (Article 17 of the Directive on Financial Reporting of SIX Swiss Exchange).

The consolidated financial statements have been prepared under the assumption of going concern for the Group’s business. Valuations in the consolidated financial statements are based on historical acquisition or production costs, unless a standard prescribes another valuation basis for an item in the financial statements or another value was used based on an accounting policy choice. This is the case for the investment properties presented in note 2.2, which were valued at fair value.

The consolidated financial statements are presented in Swiss francs (CHF), the Company’s functional currency. Unless otherwise stated, all financial information is presented in Swiss francs, rounded to the nearest thousand.

The consolidated financial statements are based on the stand-alone financial statements prepared in accordance with consistent principles as at 31 December 2020 by all group companies in which the Company directly or indirectly held more than 50% of voting rights or which it controls in another way. The entity included in the scope of consolidation together with the Company is Ina Invest Ltd.

| Share capital in CHF thousands | Votes and capital share | ||||||

| Name of the company | Domicile | Business activity | 31.12.2020 | 01.04.2020 | Inclusion in consolidated financial statements | 31.12.2020 | 01.04.2020 |

| Ina Invest Ltd | Zürich | Properties | 202 | 100 | Full consolidation | 57.5% | 50.1% |

Implenia Ltd holds the remaining voting rights and shares in Ina Invest Ltd (42.5%; 1 April 2020: 49.9%). The decrease in Implenia Ltd’s shareholding was due to the capital increase in June 2020. See note 3.4 for more information on the capital increase.

Subsidiaries are included in the consolidated financial statements from the date on which control is assumed and excluded from the date on which control is relinquished. These dates do not necessarily coincide with the acquisition or disposal date. Capital consolidation is performed according to the purchase method. This involves the group companies’ equity being offset against the carrying amount of the parent company’s investment at the time when it is purchased or, if appropriate, at the date of incorporation. Assets and liabilities of the group company are measured at fair value as at this date in accordance with principles that are consistent throughout the Group. Using the full consolidation method, the assets and liabilities of the consolidated companies were recognised in full in the consolidated annual financial statements. Intragroup assets and liabilities are eliminated, as are intragroup income and expenses.

In order to prepare the consolidated financial statements in accordance with Swiss GAAP FER, management has to make estimates, assessments and assumptions that impact the application of the accounting and valuation methods as well as the presentation and reported amounts of assets, liabilities, income and expenses. The estimates and assumptions are based on experience and various other factors that are considered relevant in the prevailing circumstances. The actual results may deviate from these estimates.

Estimates and assumptions are reviewed regularly. Changes in estimates may be necessary if the circumstances on which the estimated values are based have changed or if there is new information or additional insights. Such changes are recognised in the reporting period in which the estimate is adjusted.

Management estimates and assumptions applied in Swiss GAAP FER that may have a significant impact on the consolidated financial statements or involve a high risk of adjustment in the following year are explained in the subsequent notes:

The first-time valuation of the items promotional properties, investment properties and intangible assets (purchase rights for plots of land) was carried out at fair value pursuant to explanations in note 1.2. At the time of initial recognition as at 1 April 2020, the promotional properties and intangible assets were subject to the estimates and assumptions set out in note 2.2.

2 Operating activities

The following section presents additional information on the operating result and the current and noncurrent assets relevant to the Group’s operating activities. The notes on assets primarily concern the promotional and investment properties.

Promotional properties include projects involving condominium apartments intended for sale at a later date.

| in CHF thousands | 31.12.2020 | 01.04.2020 |

| Projects under development | 53,630 | 70,550 |

| Projects under construction | 22,370 | - |

| Projects in sale | - | - |

| Total promotional properties | 76,000 | 70,550 |

The plots of land on which the projects are being built are completely owned by Ina Invest at the beginning of a project. Ina Invest develops the plots of land until it receives a building permit for them and then makes them ready to be built on. Construction begins as soon as most of the condominium apartments have been reserved. A general contractor executes the constructions. The two projects, Ernst-Jung-Gasse 18 (Lokstadt Tender) in Winterthur and Auf der Höhe 12-18 (Am Schwinbach) in Arlesheim, have Implenia Group acting as general contractor. In terms of risks and rewards, a distinction is made between sold and unsold projects under construction as well as completed projects being sold:

- Projects under construction: During the construction phase, Ina Invest, as the owner of the plots of land, bears the material risks and rewards from the development and implementation until the units are sold to an end customer. Accordingly, acquisition cost for the plot of land and development costs attributable to the unsold units are recognised in promotional properties. When units are sold, Ina Invest transfers the relevant portion of the fully developed land to the buyer, who concludes or has already concluded an agreement with a general contractor to build the unit. Ina Invest no longer bears any risks or rewards for these units after their sale, which is why the acquisition cost for the plot of land and development cost for this unit is de-recognized at the time of the transaction and no further development costs are recognised. Investment commitments towards the general contractor for the realization of units not sold yet are disclosed in note 3.2.

- Projects in sale: For units not sold, the cost of work performed by the general contractor is transferred to Ina Invest after construction is completed. Ina Invest is obliged to accept the work provided during the construction phase. Ina Invest sells units not yet sold by the end of the construction as turnkey units to the end customers. Ina Invest bears the material risks and rewards concerning the condominium apartments between the end of construction until the sale, therefore acting as seller of the portion of the plot of land and the respective development cost share.

The following table shows the change in the number of the projects’ condominium apartments included in the promotional properties.

| In units | Projects under development | Projects under construction | Projects being sold | Total |

| Balance as at 01.04.2020 | 174 | - | - | 174 |

| Additions | 66 | - | - | 66 |

| Disposals from notarized sales | - | (3) | - | (3) |

| Transfer between categories | (39) | 39 | - | - |

| Balance as at 31.12.2020 | 201 | 36 | - | 237 |

| Of which reserved | - | 23 | - | 23 |

The additions in the reporting period result from the change in use of parts of the projects Chemin de l’Echo and Avenue des Grandes-Communes (Les Tattes) in Onex. For further information refer to note 2.2.

For details on the initial recognition at the date of the consolidated opening balance sheet as at 1 April 2020, please refer to note 1.2.

Results from the sale of promotional properties

Income from the sale of promotional properties is attributable to 3 condominium units in the project Ernst-Jung-Gasse 18 (Lokstadt Tender) in Winterthur, which were sold during the reporting year.

| in CHF thousands | 01.04.-31.12.2020 |

| Income from the sale of promotional properties | 1,399 |

| Direct expenses from the sale of promotional properties | (1,219) |

| Result from the sale of promotional properties | 180 |

Accounting policies

In promotional properties, each unit is measured at the lower of acquisition cost and fair value less cost to sell. Any impairment to the lower fair value less cost to sell is recognized in the relevant category of the item promotional properties. Any value adjustments to the lower fair value less cost as well as value recoveries on promotional properties are recognised in the result for the period.

The Projects under development category includes plots of land already owned by Ina Invest or down payments on notarised land purchases as well as any directly attributable accrued development costs if construction has not yet been started.

The capitalised acquisition costs for projects are reclassified to the Projects under construction category when construction starts. This category contains plots of land or parts thereof that have not yet been sold and that contain properties whose construction has not yet been completed.

The capitalised acquisition costs of condominium apartments not yet sold include the plot of land on which they stand, the directly attributable development costs and the accrued costs assumed under the contract for the construction work and services performed up to that point.

Unsold condominium apartments whose construction has been completed are reported under Projects in sale. Ina Invest is obliged to take over the work that the general contractor has performed under its contract for work and services. The capitalised costs comprise the plot of land, the directly attributable development costs and the costs assumed under the contract for work and services. Ina Invest sells these as turnkey units to end customers, assuming the price and sales risk for unsold units but also receiving the economic benefit from their sale.

Income from the sale of promotional properties usually are the selling price. Units sold from projects under construction generally correspond to the price attributable to the portion of the plot of land, while income from the sale of turnkey units is recognised as the selling price for the unit’s land and development cost. Proceeds resulting from the sale of plots of land or subplots as well as completed condominium apartments generally are recognised once the risks and rewards have been transferred to the buyer. This date is defined in the sales agreement (generally this is the date of transfer of ownership).

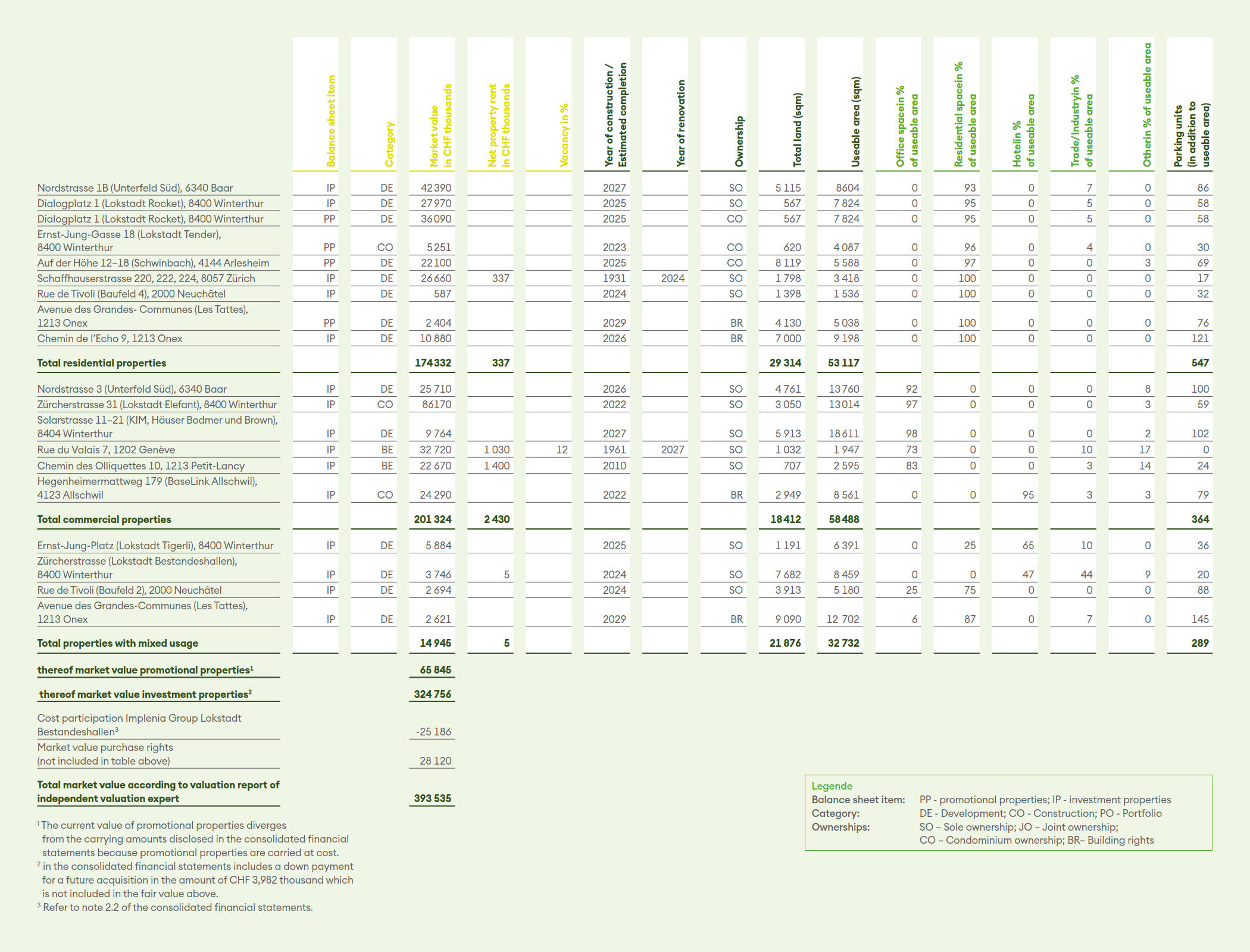

Investment properties comprise plots of land and properties that are expected to be held and managed over a longer period of time. This item includes properties under development, properties under construction and portfolio properties held for rent.

| in CHF thousands | Properties under development | Property under construction | Portfolio properties | Total |

| Cumulative acquisition costs | ||||

| Balance as at 01.04.2020 | 159,771 | - | - | 159,771 |

| Additions | 25,565 | 14,104 | 51,650 | 91,319 |

| Performance-based development fee | 492 | 1,040 | 724 | 2,256 |

| Transfer between balance sheet items | 6,265 | - | - | 6,265 |

| Transfer between categories | (47,623) | 47,623 | - | - |

| Balance as at 31.12.2020 | 144,470 | 62,767 | 52,374 | 259,611 |

| Cumulative revaluations | ||||

| Balance as at 01.04.2020 | - | - | - | - |

| Profit from revaluation | 6,853 | 3,449 | 2,896 | 13,198 |

| Loss from revaluation | (3,565) | - | - | (3,565) |

| Transfer between balance sheet items | (316) | - | - | (316) |

| Transfer between categories | (709) | 709 | - | - |

| Balance as at 31.12.2020 | 2,263 | 4,158 | 2,896 | 9,317 |

| Carrying amounts of investment properties | ||||

| Balance as at 01.04.2020 | 159,771 | - | - | 159,771 |

| Balance as at 31.12.2020 | 146,733 | 66,925 | 55,270 | 268,928 |

The contractual agreements with Implenia Group as a partner for the development of investment properties include a performance-based development fee for the services rendered (see note 4.3). This contractual arrangement applies to all investment properties in the portfolio as at the balance sheet date. The performance-based development fee corresponds to 20% of the project result between the market values and the investment acquisition costs before settlement of the performance-based development fee. For Ina Invest, this contractual mechanism can lead to an increase or also a reduction of the development costs recognised on the basis of other contractual elements. Generally, the performance-based development fee is settled after completion of the development project. Thereafter, the development partner Implenia Group has no further share of a potential increase or reduction in the value of the investment property. The performance-based development fee recognised as at 31 December 2020 resulted in non-current receivables from and non-current liabilities to the developer (see note 2.5). Without the contractually agreed performance-based development fee, the profit from revaluation would amount to CHF 16,498 thousand and the loss on revaluation to CHF 4,609 thousand. The net profit from revaluation would be CHF 2,256 thousand higher than presented in the income statement as at the balance sheet date.

Of the additions to investment properties in the amount of CHF 93,575 thousand, CHF 86,867 thousand led to a cash outflow as at 31 December 2020. The remaining amount that was capitalised and resulted in accrued expenses or liabilities with Implenia Group, which were converted to equity during the reporting period. Please see note 3.4 for the conversion of accrued expenses (as at 1 April 2020 and additions during the reporting period) into equity.

The category Properties under development includes the Lokstadt Bestandeshallen property on Zürcherstrasse in Winterthur, which has a negative market value of CHF 27,610 thousand as at 31 December 2020 due to crosssite uses (e.g. kindergarten) (1 April 2020: negative market value of CHF 27,060 thousand). These cross-site increases the attractiveness of the surrounding properties. Implenia Group has therefore contractually agreed to assume an obligation of 40% of the cost of the work supplied by the general contractor up to a maximum of CHF 27,000 thousand plus VAT. This assumption of costs is subject to conditions regarding timing and specific use and requires a contract for work and services. The current carrying amount of the investment property has been set to zero as of 31 December 2020 (1 April 2020: zero). Furthermore, a non-current provision from loss making contracts in the amount of CHF 610 thousand has been recognised in the reporting period. The amount represents the best possible estimate of the negative value that an independent third party would assign to the development property under these circumstances. The provision has been recognised in other direct operating expenses.

Valuation methods

Property valuations are carried out by Wüest Partner Ltd, Zurich, an external, independent and qualified valuation expert. The properties are valued in accordance with the discounted cash flow method (DCF method), whereby the fair value of a property is determined by the sum of the entire estimated future net income discounted to the present value. The net income (EBITDA) for each property is discounted individually taking into account property-specific risks and rewards, as well as market conditions and risks. For properties under development or under construction, the value of the project is determined in three steps:

- Valuation of the property at the time of its completion, taking into account the current occupancy rate, market and cost estimates as at the cut-off date:

- Determination of the market value as at balance sheet date, in light of the forecasted future investments;

- Estimation of the risk, taking into account the separate cash flow of a cost item.

The discounting rates, market rents and vacancy rates have been identified as material non-observable input factors. The values used are summarised below.

Non-observable input factors used as at 31 December 2020

| Information in | Properties under development | Property under construction | Portfolio properties | |

| Discount rate | ||||

| Discount rate, bandwidth | % | 2.55%-3.65% | 2.80%-3.65% | 2.60%-3.20% |

| Achievable market rents | ||||

| Office space | CHF per m2 | 205-280 | 261 | 350-602 |

| Residential space | CHF per m2 | 210-397 | n/a | 585 |

| Hotel space | CHF per m2 | 300 | 242 | n/a |

| Parking space inside | CHF per unit | 1,482-2,160 | 1,800-2,100 | 2,400 |

| Commercial/industrial space | CHF per m2 | 200-300 | n/a | 380 |

| Others | CHF per m2 | 90-265 | 50-400 | 120-130 |

| Vacancies | ||||

| Bandwidth vacancy rate | % | 1.50%- 5.00% | 5.00% | 4.20%-5.00% |

Non-observable input factors used as at 1 April 2020

| Information in | Properties under development | |

| Discount rate | ||

| Discount rate, bandwidth | % | 2.60%- 3.75% |

| Achievable market rents | ||

| Office space | CHF per m2 | 208-280 |

| Residential space | CHF per m2 | 210-397 |

| Hotel space | CHF per m2 | 240-300 |

| Parking space inside | CHF per unit | 1,482-2,160 |

| Commercial/industrial space | CHF per m2 | 200-300 |

| Others | CHF per m2 | 90-280 |

| Vacancies | ||

| Bandwidth vacancy rate | % | 1.50%- 5.80% |

Beyond that, uncertainties regarding future investments remain. Details on the valuation methods and assumptions are stated in the report by the valuation expert.

For more information on the initial recognition at the time of the opening balance sheet, please refer to note 1.2. Investment properties are subsequently measured at fair value.

Additions/transfers in the reporting period

The following additions from exercise of purchase rights and acquisitions as well as transfers resulting from changes in use took place during the reporting period:

| Property | Description | From | To |

| Rue de Tivoli (construction areas B2 and B4), 2000 Neuchâtel | Purchase rights for construction areas B2 and B4 on Rue de Tivoli, Neuchâtel were exercised in April 2020 for a consideration of CHF 3,224 thousand. | Intangible assets; category “Purchase rights and purchase commitments” | Investment properties; category “Properties under development” |

| Schaffhauserstrasse 220-224, 8057 Zürich | The purchase right for project Schaffhauserstrasse 220-224, Zurich was exercised in October 2020 for a consideration of CHF 16,000 thousand. | Intangible assets; category “Purchase rights and purchase commitments” | Investment properties; category “Properties under development” |

| Rue du Valais 7, 1202 Geneva | An already existing portfolio property was purchased for a consideration of CHF 29,031 thousand at rue du Valais 7 in Geneva in October 2020. | - | Investment properties; category “portfolio property” |

| Chemin des Olliquettes 10, 1213 Petit-Lancy | An already existing portfolio property was purchased for a consideration of CHF 23,343 thousand at Chemin des Olliquettes in Petit-Lancy in October 2020. | - | Investment properties; category “portfolio property” |

| Chemin de l’Echo 9, 1213 Onex | In view of a change in laws in the Canton of Geneva, which stipulates that a part of the property must consist of condominiums, a part of the property Avenue des GrandesCommunes (Les Tattes) in Onex was transferred from investment properties to promotional properties. | Investment properties; category “Properties under development” | Promotional properties; category “Projects under development” |

| Avenue des Grandes-Communes (Les Tattes), 1213 Onex | In view of a change in laws in the Canton of Geneva, which stipulates that a part of the property must consist of condominiums, a part of the property Chemin de l’Echo in Onex was transferred from investment properties to promotional properties. | Investment properties; category “Properties under development” | Promotional properties; category “Projects under development” |

The following properties are re-allocated between categories within investment properties:

| Property | From | To |

| Zürcherstrasse 31 (Lokstadt Elefant), 8400 Winterthur | Properties under development | Properties under construction |

| Hegenheimermattweg 179 (Baselink Allschwil), 4123 | Properties under development | Properties under construction |

Encumbered investment properties

During the reporting period, collateral for a mortgage note used to finance a project was issued, thus encumbering the investment properties located at Schaffhauserstrasse 220-224 in Zurich and at Zürcherstrasse 31 (Lokstadt Elefant) in Winterthur. The recognised fair value of these two properties amounted to CHF 84,440 thousand as at 31 December 2020. As at balance sheet date, the credit facility remained undrawn. See note 3.1 for more information.

Significant Management assumptions and estimates

The investment properties have been valued at fair value, which correspond to the expected income, respectively cash flow discounted by applying a risk-adjusted discount rate. The valuations are based on different significant estimates and assumptions, such as the achievable market rents, the expected vacancy rates and the discount rate. Projects under development also require estimates and assumptions regarding future investments, permits and project timelines. Changes in these estimates and assumptions may cause material changes in the values recognised in the balance sheet.

The impact of COVID19 had already been factored into the property valuations as at 1 April 2020. In the valuations of 31 December 2020, the market prospects and uncertainties resulting from COVID-19 have again been incorporated into the assumptions. Ina Invest’s portfolio is geared to the long term, and a large portion of it consists of residential real estate. As expected, no effects could be determined that could be attributed directly to COVID-19 between 1 April 2020 and 31 December 2020. Should the assumptions and estimates change in this regard, there may also be significant changes in the values recognized in the balance sheet.

Accounting policies

The initial recognition is at acquisition cost including directly attributable costs. Acquisition costs include an estimate of the recognised part of the performance-based development fee to which the developer is contractually entitled. The property valuations prepared by the independent valuation expert form the basis of the estimate. Investments for replacements and expansions are capitalised if they are likely to generate future economic benefits for Ina Invest. This is generally the case if the market value or the value in use increases substantially or if the useful life is significantly extended.

Investment properties are subsequently measured at fair value, provided the value can be determined reliably. As a rule, this will be the case as soon as a specific project exists. If the fair value of a property cannot be determined reliably, it is recognised in the balance sheet at acquisition cost less any impairment. Changes in the fair value are recognised through profit or loss. The net income from revaluation of the investment properties is attributable to changes in their fair values.

Properties under development comprise undeveloped plots of land and properties where comprehensive work is planned. Construction, renovation or repurposing plans are prepared for these properties. The Properties under construction category consists of properties where a building permit has been granted and construction has already begun. Properties are reclassified to this category once construction starts. When a building is (partially) opened, it is transferred to the “Portfolio properties” category. Portfolio properties consists of properties which are held rented over a longer period of time or whose development is planned for the long-term.

| in CHF thousands | Purchase rights and purchase commitments | Total |

| Cumulative acquisition costs | ||

| Balance as at 01.04.2020 | 27,404 | 27,404 |

| Additions | 223 | 223 |

| Transfer between balance sheet items | (6,451) | (6,451) |

| Balance as at 31.12.2020 | 21,176 | 21,176 |

| Cumulative impairments | ||

| Balance as at 01.04.2020 | - | - |

| Balance as at 31.12.2020 | - | - |

| Carrying amount of intangible assets | ||

| Balance as at 01.04.2020 | 27,404 | 27,404 |

| Balance as at 31.12.2020 | 21,176 | 21,176 |

Of the additions to intangible assets in the amount of CHF 223 thousand, CHF 13 thousand led to a cash outflow as at 31 December 2020. The remaining amount that was capitalised resulted in accrued expenses or financial liabilities with Implenia Group, which were converted to equity during the reporting period. Please see note 3.4 for the conversion of accrued expenses (as at 1 April 2020 and additions during the reporting period) into equity.

The purchase rights for the construction areas B2 and B4 at Rue de Tivoli, Neuchâtel were exercised in April 2020. Moreover, purchase rights were exercised to acquire Schaffhauserstrasse 220-224, 8057 Zurich in October 2020. These two transactions resulted in a transfer to investment properties. For further information on these transactions, see note 2.2.

As at 31 December 2020, intangible assets include the purchase rights for plots of land located at Rue du Château in Préverenges (plot size: 2,763 m2). The execution of the purchase right shall take place when the neighbourhood plan becomes legally effective, but no later than 28 February 2025.

Purchase rights disclosed as intangible assets correspond to acquisition costs for purchase rights or purchase commitments. The nominal amount of non-recognizable commitments arising from purchase commitments amounts to a total of CHF 5,007 thousand (1 April 2020: CHF 24,230 thousand).

For more information on the initial recognition at the time of the opening balance sheet, please refer to note 1.2.

Accounting policies

Intangible assets are identifiable, non-monetary assets without physical existence. Intangible assets are recognised in the balance sheet at acquisition or production costs less accumulated amortization and impairment.

In the case of purchase rights, Ina Invest acquires the right to purchase a plot of land. The payment of purchase rights as well as accrued development services by third parties and own services are recorded as intangible assets, provided there is contractual evidence of acquiring the plot of land but the plot has not yet passed into the ownership of Ina Invest. Purchase rights and purchase commitments for properties are recognised at acquisition costs. They are not amortised subsequently as the purchase rights are not used during the useful life and as the underlying land parcels are not subject to wear and tear.

Intangible assets are subject to an impairment test at each sheet date. If there is an indication that intangible assets could be impaired, the recoverable amount is determined. The recoverable amount is the higher of the net selling price and the value in use. Should the carrying value of the asset exceed the recoverable amount, an impairment is recorded in the result for the period. Reversal of past impairment losses are recognised in the result for the period.

Accrued expenses and deferred income amounting to CHF 1,439 thousand as at 31 December 2020 mostly consist of non-invoiced costs from development services, capital taxes, accounting and consultation services accrued during the reporting period.

All of the accrued expenses and deferred income amounting to CHF 34,398 thousand as at 1 April 2020 are accrued expenses to the affiliated Implenia Group. In the course of transferring development projects to Ina Invest Ltd, accrued expenses arose for site and development costs. During the capital increase of the subsidiary, Ina Invest Ltd, that took place on 17 June 2020, accrued expenses in the amount of CHF 40,131 thousand were converted to equity. For further information, please refer to note 3.4.

Accounting policies

Accrued expenses are recognised and measured at nominal value.

| in CHF thousands | 31.12.2020 | 01.04.2020 |

| Receivables from perfomance-based development fee | 1,044 | - |

| Total other non-current receivables | 1,044 | - |

| in CHF thousands | 31.12.2020 | 01.04.2020 |

| Payables from performance-based development fee | 3,300 | - |

| Payables from development costs for properties | 1,131 | - |

| Total other non-current liabilities | 4,430 | - |

Receivables and payables from the performance-based development fee have resulted from the contractually agreed variable development fee of Implenia Group. For further information, please refer to notes 2.2 and 4.3.

Accounting policies

Receivables and payables from the performance-based development fee are measured at the estimated fair value. Other non-current liabilities are recognised and measured at nominal value.

During the reporting period, Ina Invest generated rental income from investment properties amounting to CHF 791 thousand. This rental income is attributable to the three investment properties located at Chemin des Oliquettes 10 in Petit-Lancy, Rue du Valais 7 in Geneva and Schaffhauserstrasse 220-224 in Zurich.

| in CHF thousands | 01.04.-31.12.2020 |

| Rental income from properties | 791 |

| Direct rental expenses | (69) |

| Result from rental of properties | 722 |

Maturity of long-term rental agreements

This maturity schedule shows the terms of commercial rental agreements (e.g. for hotels, commercial and industrial uses). Rental income from residential properties is not included as these agreements may be terminated on a short-term notice.

| in CHF thousands | 31.12.2020 |

| Rental income within 1 year | 2,303 |

| Rental income within 2 to 5 years | 14,523 |

| Rental income after 5 years | 38,899 |

| Total future rental income from perpetual leases (without residential properties) | 55,726 |

Most important tenants

The rental income of the following five most important tenants accounts for 63.1% of the entire target rental income during the reporting period.

| in % | 01.04.-31.12.2020 |

| SA Régie du Rhône | 41.1% |

| Mission Permanente de l'Inde | 12.0% |

| Genèveroule | 3.6% |

| Fondation Suisse du Service Social International | 3.2% |

| Guinée - Mission Permanente | 3.2% |

| Total | 63.1% |

Rental losses due to vacancies

Rental losses due to vacancies in portfolio properties amounted to CHF 13 thousand during the reporting period, which corresponds to a vacancy rate of 1.4% (comparing vacancies to target rental income).

Accounting policies

Rental income from the letting of properties represents net rental income, i.e. target rental income less rental losses and vacancy losses.

Rental agreements are operating leases. Rental income is recognised in the income statement on an accrual basis over the lease term. If tenants are granted significant rent incentives (e.g. rent-free periods), the equivalent value of the incentive is recognised on a straight-line basis over the entire term of the lease as an adjustment to income from rentals.

Ina Invest is currently only active on the Swiss market. The property portfolio, comprising promotional and investment properties, is managed as a single entity by the Board of Directors and Executive Management. In accordance with Swiss GAAP FER 31, the Group therefore has a single segment. Therefore, no segment report is presented.

| in CHF thousands | 01.04.-31.12.2020 |

| Capital increase cost | (2,007) |

| Accounting and consultation fees | (806) |

| Capital taxes | (460) |

| Interest expenses related to building leases | (95) |

| Marketing | (94) |

| Administrative expenses | (81) |

| Other operating expenses | (61) |

| Total other operating expenses | (3,604) |

The capital increase costs recognised in profit or loss for the period are costs that are not directly related to the actual transaction of the capital increase. This includes, for example, legal advisory expenses, expenses for project management and project support by external service providers.

3 Financing

This section contains information on the financing of the Group through debt and equity.

| in CHF thousands | Currency | Interest rate | Maturity | 31.12.2020 | 01.04.2020 |

| Loans with related parties | CHF | 2.25% | 31.12.2021 | - | 20,000 |

| Total loans | - | 20,000 | |||

| Of which current | - | 20,000 |

In the course of the asset transfer as at 1 April 2020, Implenia Group granted Ina Invest Ltd a loan amounting to CHF 20,000 thousand. The loan was reported as a current financial liability due to the termination option.

In the course of Ina Invest Ltd’s capital increase on 17 June 2020, CHF 19,126 thousand of this loan was converted into equity in Ina Invest Ltd. This transaction had an impact on the minority interests of Implenia Group. For further information, please refer to note 3.4. The remaining portion of CHF 874 thousand was repaid during the reporting period.

During the reporting period, Ina Invest concluded two framework credit agreements at the following terms and conditions:

| Investment properties | ||

| 31.12.2020 | 01.04.2020 | |

| Amounts of credit framework in CHF thousands | 85,600 | - |

| Property liens in CHF thousands | 85,600 | - |

| Credit sum drawn down as at balance sheet date in CHF thousands | - | - |

| Maturity period | perpetual | - |

| Interest rate | Variable, not determined yet | - |

For further information on property liens, please refer to note 2.2.

Accounting policies

Financial liabilities are initially recognised at fair value less directly attributable transaction costs. Subsequently, they are measured at amortised cost using the effective interest rate method.

Financial liabilities due within 12 months of the balance sheet date are classified as current financial liabilities.

As at 31 December 2020, the Group has off-balance sheet commitments arising from agreements concluded with Implenia Group in relation to future developments and construction investments amounting to CHF 106,400 thousand (1 April 2020: CHF 130,824 thousand).

| in CHF thousands | 31.12.2020 | 01.04.2020 |

| Promotional properties | 49,206 | 56,383 |

| Investment properties | 57,194 | 74,441 |

| Total non-recognisable commitments from future development and construction investments | 106,400 | 130,824 |

Furthermore, Ina Invest has commitments for non-recognisable leases amounting to CHF 116,854 thousand as at 31 December 2020 (1 April 2020: CHF 116,949 thousand) arising from building leases with a residual term to maturity of about 36 to 99 years. CHF 116,005 thousand (1 April 2020: 116,190 thousand) of which are due in more than five years.

Accounting policies

In the case of an agreement to use the plots for which building leases interest is paid, the company shall assess whether the expenditure should be classified as operating lease or finance lease. Payments made for an operating lease are recognised in the income statement for the duration of the lease or the leasehold.

Each financial year, Implenia Group may sell up to 5% of its investment in Ina Invest Ltd to Invest Holding Ltd (put option). In doing so, the company may decide whether it prefers cash or Ina Invest Holding shares in consideration. If Implenia Group exercises the put option, the sales price will equal the implicit market value of Ina Invest Ltd. The implicit market value will be determined based on the share price of Ina Invest Holding Ltd. The value of the associated contingent liability is estimated at CHF 119,599 thousand as at 31 December 2020 (1 April 2020: CHF 82,496 thousand).

Accounting policies

Payment commitments to minority shareholders arising from their put options for the corresponding minority interests are equivalent to contingent liabilities and are therefore not recognised in the balance sheet.

Share capital

The share capital of the parent company, Ina Invest Holding Ltd, amounts to CHF 265,997 as at 31 December 2020 (1 April 2020: CHF 110,832) and consists of 8,866,560 registered shares with a nominal value of CHF 0.03 each (1 April 2020: 3,694,400 registered shares with a nominal value of CHF 0.03 each). A capital increase was carried out when the Company went public on 12 June 2020, creating 5,172,160 new shares with a nominal value of CHF 0.03 each, which have been fully paid up.

Shareholders are entitled to receive the fixed dividends as well as one vote per share at the Company’s Annual General Meeting.

Authorised share capital

In accordance with the Company’s Articles of Association, the Board of Directors is entitled to increase the share capital by a maximum of CHF 53,199.36 at any time until 2 June 2022 by issuing up to 1,773,312 registered shares with a nominal value of CHF 0.03 each, which are to be fully paid up.

Several increases, each worth part of this amount, are permitted. The Board of Directors determines the issue price, the type of contributions, the timing of the issue, the criteria for exercising subscription rights and the time at which a dividend entitlement starts to apply. In the case of a capital increase from authorised capital, the Board of Directors is entitled to withdraw or restrict shareholders’ subscription rights up to a maximum of 886,656 registered shares provided certain criteria set out in the Articles of Association are met.

Conditional share capital

In accordance with the Company’s Articles of Association, the conditional share capital can be increased by a maximum of CHF 13,299.84 by issuing up to 443,328 registered shares with a nominal value of CHF 0.03 each, which are to be fully paid up. Such an increase is to be carried out by exercising option rights granted to employees or members of the Board of Directors of the Company or group companies.

Capital reserves and minority interests in equity

The capital reserves correspond to the difference between, on the one hand, the monetary contributions and contributions in kind made by shareholders as valued in accordance with the provisions of Swiss GAAP FER and, on the other hand, the nominal values of the shares received associated with the respective stages of contribution. Moreover, in accordance Swiss GAAP FER, share-based compensations are recognised in capital reserves (see note 4.2). Due to valuation differences the capital reserves reported in the consolidated balance sheet are not identical to the capital reserves in accordance with the Company’s separate financial statements.

The impact of the capital increase of 12 June 2020 on the Company’s equity is presented below:

| in CHF thousands | Share capital | Capital reserves | Retained earnings | Share- holders’ equity | Minority interests | Total equity |

| Other capital increase expenses | 155 | 112,972 | - | 113,127 | - | 113,127 |

| Proceeds from capital increase | - | (2,383) | - | (2,383) | - | (2,383) |

| Capital increase | 155 | 110,589 | - | 110,744 | - | 110,744 |

On 17 June 2020, Ina Invest Ltd increased its capital, in which Implenia Ltd also participated as a minority shareholder. Ina Invest Holding Ltd. invested CHF 108,940 thousand in Ina Invest Ltd. During the capital increase, the capital and voting rights share of Implenia Ltd in Ina Invest Ltd were reduced from 49.9% to 42.5%. The transaction’s impact on the Company’s equity is presented in the following overview:

| in CHF thousands | Aktien-kapital | Capital reserves | Retained earnings | Share- holders’ equity | Minority interests | Total equity |

| Conversion of accrued expenses with Implenia Group | - | - | - | - | 40,131 | 40,131 |

| Conversion of loan with Implenia Group | - | - | - | - | 19,126 | 19,126 |

| Capital increase costs | - | (1,106) | - | (1,106) | (818) | (1,924) |

| Income tax on capital increase expenses | - | 213 | - | 213 | 157 | 370 |

| Re-allocation | - | 3 | - | 3 | (3) | - |

| Capital increase subsidiaries | - | (890) | - | (890) | 58,593 | 57,703 |

The capital contributions made by the Company’s shareholders and the minority shareholder did not fully match the new shareholding ratios, which resulted in a re-allocation.

In the reporting period, costs of CHF 9,146 thousand were incurred in connection with capital increases, of which CHF 7,139 thousand were recognised in equity and CHF 2,007 thousand were charged to the income statement. Of the capital increase costs recognised in equity, CHF 2,832 thousand were netted directly against the proceeds from the capital increase; the net amount was then transferred to Ina Invest. The item was presented in the cash flow statements under proceeds from capital increase.

Treasury shares

| Ø transaction price in CHF | Number of registered shares | Portfolio in CHF thousands | |

| Balance as at 01.04.2020 | - | - | |

| Acquisition of treasury shares | 17.42 | 9,500 | 165 |

| Balance as at 31.12.2020 | 9,500 | 165 |

The transaction price always corresponded to the market price.

Accounting policies

Directly attributable transaction costs from equity transactions such as capital increases are recognised in equity as a reduction in capital reserves after deducting the associated income tax.

Treasury shares are recognised at acquisition cost at the date of acquisition. In case of a resale, the gain or loss incurred is recognised in the capital reserves.

| in CHF thousands | 31.12.2020 | 01.04.2020 |

| Promotional properties | 76,000 | 70,550 |

| Investment properties | 268,928 | 159,771 |

| Intangible assets (purchase rights) | 21,176 | 27,404 |

| Total value of property portfolio | 366,104 | 257,725 |

| Cash and cash equivalents | 14,118 | 1,202 |

| Trade accounts receivable | 453 | - |

| Other current receivables | 1,174 | - |

| Accrued income and prepaid expenses | 1,295 | - |

| Other non-current receivables | 1,044 | - |

| Current financial liabilities | - | (20,000) |

| Trade accounts payable | (56) | |

| Advance payments for promotional properties | (460) | - |

| Other short-term liabilities | (108) | - |

| Accrued expenses and deferred income | (1,439) | (34,398) |

| Deferred tax liabilities | (39,496) | (39,208) |

| Other non-current liabilities | (4,430) | - |

| Non-current provisions | (610) | - |

| NAV (equity including minorities) | 337,589 | 165,322 |

| NAV (equity excluding minorities) | 194,036 | 82,826 |

| NAV (shareholders' equity excluding minorities) per share (in CHF) | 21.91 | 22.40 |

As at 31 December 2020, earnings per share are calculated as follows:

| In CHF thousands, as indicated | 01.04.-31.12.2020 |

| Profit attributable to shareholders of Ina Invest Holding Ltd | 1,394 |

| Weighted average number of shares outstanding | 7,513,045 |

| Earnings per share (in CHF) | 0.19 |

| Profit attributable to shareholders of Ina Invest Holding Ltd | 1,394 |

| Weighted average number of shares outstanding | 7,515,172 |

| Diluted earnings per share (in CHF) | 0.19 |

4 Other disclosures

This section contains information that has not already been disclosed elsewhere in the consolidated annual financial statements.

Income tax expenses

Income tax expenses are composed of the following:

| in CHF thousands | 01.04.-31.12.2020 |

| Current year income taxes | 82 |

| Deferred income taxes | 659 |

| Total income taxes | 740 |

The average applicable tax rate based on the ordinary result is 21.1% (1 April 2020: 19%). The reasons for the deviations from the effective tax burden are as follows:

| in CHF thousands | 01.04.-31.12.2020 |

| Earnings before income taxes | 4,598 |

| Expected income tax rate | 21.1% |

| Expected income taxes | 972 |

| Taxes at other rates (incl. property gains taxes) | (666) |

| Effects from non-capitalised tax losses carried forward | 1,537 |

| Other effects | (1,103) |

| Effective income taxes | 740 |

| Effective income tax rate | 16.1% |

The other effects amounting to CHF 1,103 thousand result from capital increase costs recognised in profit or loss in the Company’s tax accounts, which were offset against equity in the consolidated financial statements. The reconciliation item results from the separate presentation of non-capitalised tax losses carried forward incurred in the reporting period (gross presentation of effects).

Deferred tax liabilities and deferred tax assets

| in CHF thousands | 01.04.-31.12.2020 |

| Deferred tax liabilities as at 01.04.2020 | 39,208 |

| Increase from revaluations and depreciation | 1,421 |

| Capitalised tax losses carried forward | (1,133) |

| Deferred tax liabilities as at 31.12.2020 | 39,496 |

If a revaluation in the consolidated balance sheet in comparison to the tax values involved recoverable write-offs, the taxes were segregated for each property after deducting any property gains tax and considered separately. For this, income tax rates ranged between 12% and 20% (1 April 2020: 12% to 20%).

Two different taxation systems are used if revaluations exceed the recoverable write-offs. In cantons that do not foresee any special taxation, the taxes are also calculated with the tax rates mentioned above. Other cantons levy separate property gains tax ranging from 20% to 40% (1 April 2020: 20% to 47%), depending on the duration of ownership plus direct federal taxes of 7.83%.

Ina Invest generally expects the duration of ownership to be at least 20 years, which is why no speculation surcharges have been considered. In the case of promotional property, the actual holding period up to the date of sale is considered.

During the reporting period, deferred tax assets amounting to CHF 1,133 thousand were recognised on tax losses carried forward as it seems likely that these may be netted with future profits. Deferred tax assets were netted with deferred tax liabilities. For tax losses carried forward amounting to CHF 7,266 thousand, no deferred taxes assets were recognised as it is not considered likely that they can be netted with future profits. Tax losses carried forward expire within 7 years.

Significant Management assumptions and estimates

In certain cantons, the taxation of profits from the sale of a property is subject to a special property gains tax. The level of the relevant tax rate depends on the property’s holding period and may vary greatly. Should the actual holding period for the properties differ from the expected holding period, this will produce a tax burden that diverges from the accrued deferred tax liabilities once the sale has gone through.

Accounting policies

Income taxes include all current and deferred income taxes. Current year income taxes are determined based on the taxable results. Deferred income taxes are calculated based on the temporary differences between Swiss GAAP FER balance sheet items and the values indicated in the tax balance sheet, i.e. the view depends on the balance sheet. Deferred taxes are calculated using the expected tax rates applicable and the property gains tax on properties sold.

Deferred tax credits for temporary differences which may be deducted and tax losses carried forward are only recognised to the extent that it is probable that future taxable profit will make such a claim possible. Deferred tax assets are reviewed as at every balance sheet date and reduced to the point where it is no longer likely that the relevant tax benefit can be realised.

Current year and deferred income tax liabilities and assets are netted if they are levied by the same tax authorities and pertain to the same taxable entity.

Personnel expenses and pension schemes

| in CHF thousands | 01.04.-31.12.2020 |

| Wages and salaries | (532) |

| Share-based payments | (127) |

| Pensions expenses | (49) |

| Social security expenses | (61) |

| Other personnel expenses | (21) |

| Total personnel expenses | (789) |

In the reporting period, Ina Invest employed one employee who was enrolled in the legally independent defined contribution pension plan, Implenia Vorsorge. This pension plan provides benefits in case of retirement, death or disability. It is financed through contributions made by the employer and the employee. These contributions are calculated as a percentage of the insured salary. The most current available funded status of the pension fund, Implenia Vorsorge, amounted to 119.9% as at 31 December 2019. As at this cut-off date, the pension plan was overfunded. Ina Invest does not expect any significant changes in the financial situation of Implenia Vorsorge. As at the balance sheet date, there was neither an economic benefit nor an economic obligation. As at 31 December 2020, there were neither payables nor receivables to/from the pension scheme (1 April 2020: zero).

Share-based payments

The members of the company’s Board of Directors receive an annual lump-sum compensation for their services, depending on their function. The Board of Directors’ remuneration is paid to two-thirds in cash and to one-third in blocked shares of Ina Invest Holding Ltd. The shares allocated to Board members remain blocked for three years after they have been allocated. However, they are endowed with voting rights and the right to draw dividends. In order to calculate the number of shares to be allocated to each Board member, the company takes the average Ina Invest Holding Ltd share price in the month of December of the relevant year in office. The allocation of a total of 8,084 shares took place on 4 January 2021.

The remuneration of Management (CEO) consists of a base salary in cash and a performance-related variable component from the Short-Term Incentive Plan (STIP). 50% of the STIP payment is paid in cash and 50% in Restricted Share Units (RSUs). These are usually allocated in February of the calendar year after the reporting period. For each RSU the holder is granted one registered share in Ina Invest Holding Ltd on the third anniversary of the granting. A CEO leaving the company between the grant date and the third anniversary is entitled to receive a pro rata number of RSUs. In order to calculate the number of allocated RSUs as at the balance sheet date, the prevailing average Ina Invest Holding Ltd share price is taken for the month of January after the balance sheet date. The assumed allocation of 2,920 RSUs is an estimate of the remuneration for the purpose of the accounting based on the relevant average share price as at 31 December 2020.

The lump-sum payment of the Board of Directors in shares and the STIP portion for the CEO which is paid in RSUs are equity-settled share-based payments. Expenses related to the share-based payments are recognised over the vesting period. In the case of a Board member, this is one year of service. Expenses related to CEO’s STIP are recognised over a period beginning with the start of the business year when the services were rendered and ending on the third anniversary after the RSUs have been granted.

Accounting policies

Personnel expenses are recognised in the period, in which the services were rendered.

Whether a pension scheme has an over- or underfunding is determined from its annual financial statements prepared in accordance with Swiss GAAP FER 26. An economic obligation is recognised as a liability if the conditions for creating provisions are fulfilled. An economic benefit is capitalised if Ina Invest can use it for future pension plan contributions. Personnel expenses comprise the employer contributions accrued for the period as well as any effects due to changes in any economic benefits or economic obligations.

Share-based payments paid with equity instruments are valued at their fair value prevailing on the day of the grant and recognised as personnel expenses and in equity over the vesting period. The grant date fair value is determined using valuation models used for the registered shares’ market rates at the grant date.

Besides the company’s Board of Directors and Management, Implenia Ltd and organisations controlled by it (jointly known as “Implenia Group”) are deemed to be related parties.

Ina Invest maintains a strategic partnership with Implenia Group, which is why it has concluded several long-term agreements with Implenia ending on 31 December 2030. These agreements refer to the investment in Ina Invest Ltd, financing, the development portfolio as well as the development and construction projects of Ina Invest.

List of the most important agreements with related parties

| Agreement | Description | Most important terms and conditions |

Shareholders’ agreement

| On 26 May 2020, Ina Invest Holding Ltd., Implenia Ltd. and Ina Invest Ltd. concluded a shareholders’ agreement regarding the shares of Ina Invest Ltd. The shareholders’ agreement may be terminated by any party with a notice period of 6 months as at the end of every calendar year, with the first possible termination being 31 December 2030. | The most important aspects of the shareholders’ agreement are:

|

| Portfolio management service agreement | On 26 May 2020, Ina Invest concluded a service level agreement with Implenia Real Estate Services Ltd. The agreement may be terminated by any party with a notice period of a year, with the first possible termination being 31 December 2030. | The agreement addresses the scope of services, which Implenia Real Estate Services Ltd is to render.

However, the authority to select and decide on the scope of services remains with Ina Invest |

| Master agreement for development cooperations and realisations | On 26 May 2020, Ina Invest concluded a master agreement with Implenia Immobilien Ltd and Implenia Schweiz Ltd that began retroactively from 1 May 2020. The master agreement addresses general terms and conditions of the parties’ collaboration when developing real estate; Ina Invest applies these in full to contracts or realisation agreement with Implenia Schweiz Ltd. The master agreement may be terminated by any party with a notice period of one year, with the first possible termination being 31 December 2030. | The conditions applicable to the collaboration on the development of real estate essentially include:

In addition to the fees mentioned above, Implenia Immobilien Ltd receives a performance-based development fee of 20% of the project results (positive and negative contribution). |

As is regulated by the master agreement mentioned above, Implenia Group generally has the right to “first call” the general contractor service contracts with Ina Invest Ltd at defined target costs. Target costs are determined by an independent third-party expert, taking into consideration the targeted yield defined by Ina Invest Ltd. By signing a general contractor agreement, Implenia Group grants Ina Invest Ltd the right to total transparency of its construction cost accounts. Should Implenia Group waive its right to conclude a general contractor agreement at the price stipulated or if Ina Invest Ltd’s Board of Directors can credibly demonstrate legitimate corporate interest that another company should do it, the construction agreement is tendered.

Transactions with related parties

The following list shows the amounts included in balance sheet held towards related parties. The balances resulted from services under the portfolio management service agreement, the master agreement for development cooperation and realisation and project specific agreements.

in CHF thousands

| 31.12.20 | 01.04.20 |

| Accrued income | 1,262 | - |

| Other non-current receivables | 1,044 | - |

| Financial liabilities | - | (20,000) |

| Accrued expenses | (552) | (34,398) |

| Other non-current liabilities | (4,430) | - |

Promotional properties, investment properties and intangible assets arising from the development cooperation were capitalised during the reporting period. The amounts disclosed for promotional properties in the following were reduced by the de-recognised acquisition costs that arose in connection with sales of promotional properties. Transfers between balance sheet items take into account the entire capitalised amount of the balance sheet item in which the property is disclosed as at the balance sheet date.

| in CHF thousands | 01.04.-31.12.2020 |

| Promotional properties | 7,042 |

| Investment properties | 21,247 |

Intangible assets | 38 |

The following list shows the expenses included in the income statement resulting from transactions with related parties. They resulted from services under the portfolio management service agreement.

in CHF thousands

| 01.04.-31.12.2020 |

| Other operating expenses | (1,407) |

| Financial expenses | (208) |

Accounting policies

Related parties are deemed to be those who could have a significant influence on financial and/or operating decisions of Ina Invest Ltd. This is true for board members, members of management, significant shareholders with voting rights above 20% as well as pension plan schemes. Transactions executed at conditions that are not at arms’ length are disclosed separately in the consolidated financial statements. This could include transactions without a price, such as making available know-how or transferring results of research and development.

The transfer of assets on 1 April 2020 and the conversion of accrued expenses into shareholder’s equity on 17 June 2020 resulted in transactions not affecting cash and cash equivalents in the reporting period.

In the reporting period, a fixed-term deposit with a maturity of more than 90 days was concluded which was also du in the reporting period. This resulted in payments from investments into securities and proceeds from disposals of securities in the amount of CHF 30,000 thousand each.

Cash and cash equivalents

Cash and cash equivalents include bank balances with a residual term of a maximum of 90 days. These are measured and recognised at nominal value.

Trade account receivables and other short-term receivables

Receivables are recognised in the balance sheet at nominal value less impairments required for business management reasons. Material receivables are valued individually. An impairment is made for the remaining receivables based on historic data.

Accrued income and prepaid expenses

Accrued income and prepaid expenses are recognised and measured at nominal value.

Trade accounts payable, other short-term liabilities and advance payments for promotional properties

Trade accounts payable, other short-term liabilities and advance payments for promotional properties are recognised and measured at nominal value.

{kind=link}